Are you getting the most out of your management information system?

This article first appeared in Professional Adviser.

All businesses wrestle with the productivity conundrum, but for financial advice firms, the problem is particularly acute.

Within many IFA practices, priorities are still created by individual advisers, buried in their own spreadsheets and inboxes. As a result, advisers must devote considerable headspace to administration and diary management, rather than the business of planning and client service. This siloed approach creates a danger of important tasks being missed and team members being less productive than they should be.

Using a proprietary dedicated system – to re-engineer the back office can help resolve these problems and super-charge efficiency throughout an IFA business. If your firm has such a system in place, or is considering implementing one, then there are five questions to ask yourself to ensure you’re getting maximum value from it.

- Are my processes as streamlined as they could be?

Manual workflows are often hidden, with each adviser reliant on their own spreadsheets and diaries.

Creating a series of virtual work streams – such as client reviews, protection, new business etc. – each underpinned by a series of tasks and reminders for different members of the team provides a much more granular view of the status of every client and adviser.

Having this visibility on each case makes it far easier for the management team to achieve a high level business perspective and drive consistency across operations. Meanwhile, not being reliant on advisers telling them what needs to be done minimises the chances of deliverables being missed.

- Are we helping advisers keep on top of their work?

With clear workflows in place, advisers can see all their work in progress. Any good management information system will allow you to create regular notifications for your team to help them set priorities.

When being smart with workflows, it becomes nearly impossible for an adviser to miss outstanding tasks. You also help them in their dealings with clients. If a client contacts an adviser to request an update for example, the adviser has a full audit trail at their fingertips, rather than scrabbling through notes and spreadsheets, or firing off frantic emails to the administration team.

Workflows and notifications can be particularly beneficial when it comes to annual reviews. When set up correctly, advisers can receive reminders of reviews a month (for instance) before they are due, along with any actions that need to be fulfilled for that client – do they need to arrange a valuation report or a meeting venue for example?

This allows advisers to look effortlessly efficient in front of their clients, with all their details and status at the touch of a button.

- Am I in control of adviser pipelines?

With most management information systems, you are able to see the status of each work stream – be that pre-report, at report, processing and so on. This means it is possible to see how much money has been paid, how much is due and how much on its way, split by adviser and by work stream. You also have the ability to see the percentage of revenues coming out of reviews, new business or ad hoc requests for existing clients.

In essence, management can obtain a comprehensive sales report at the click of a finger, without the need for a sales manager.

- Am I aware of potential sticking points?

By automating routine tasks and removing the administrative burden, there is potential to create a significant boost in productivity.

The knock on impact of this is that you vastly increase your team’s capability and are able to allocate resources more effectively. It also helps highlight potential problem areas. If you use timesheets for instance, you might find that senior advisers are spending time on tasks that it would make more sense to be completed by more junior members of the team.

Being aware of potential sticking points means that team-wide meetings instantly become more productive, focussed on real problems and how these can be improved or ironed out.

Of course, some might criticise management information systems as being too prescriptive, but in reality, no-one is telling the advisers what to do minute by minute. When used smartly, the upside is significant: advisers can take holiday or sick leave without worrying endlessly about the status of their clients. They have clear measures for productivity and are relieved of some of the more tedious aspects of their job.

Putting processes in place to gather and analyse management information helps to create a better, more productive business. This creates benefits for advisers and clients alike.

Six skills successful modern financial advisers share

This article first appeared in Professional Adviser

The six skills successful modern financial advisers share

What was the first thing you bought from Amazon? If, like me, you remember the days when it was one of the few online bookshops, the chances are it was the latest bestseller that introduced you to Jeff Bezos’ business.

Now think about the last thing you bought. These days it could be almost anything, from tomato ketchup to the latest games console – and you may not have even opened the app, since a talking piece of tech in your kitchen can place the order for you.

In many ways, financial advice has seen the same evolution. A decade ago, a client would call into the office to undertake a transaction – perhaps taking out a SIPP or another investment – you would make the arrangements and take the fee, and the client would go home happy with the outcome.

These days, however, advisers must be much more than transactional sellers if they are to be successful. By offering a significantly wider range of services, most have developed much deeper relationships, often acting like their clients’ own Alexa when it comes to answering questions around financial planning.

There are a handful of key traits that make a successful modern financial adviser.

A good collaborator

Professional advice is now more interconnected than ever. Most clients are likely to be working closely with their financial adviser as well as a couple of other professionals, such as an accountant and solicitor.

In today’s market, it’s hard to be successful in your own bubble. Clients are increasingly looking for a one-stop shop, and so it’s worth building a network of trusted connections you can work with to offer a full spectrum of services.

A good listener

When a client starts talking, it’s easy to make immediate judgements about how you can help them.

Those who can genuinely sit back and listen, develop much more meaningful relationships with clients. It’s vital to be able to listen to someone’s problems, goals and aspirations, using the right mix of emotional intelligence and financial knowledge to give the recommendations that best suit their individual circumstances.

As more and more automated services come to market, and robo-advice becomes more common, this ability to listen is going to prove an ever more crucial way for financial advisers to differentiate themselves and add measurable value.

Creative in communication

In uncertain times like these, maintaining clients’ trust and staying in regular contact becomes even more important.

Regular meetings are essential, but it’s worth thinking about other ways to engage and provide insight on the issues affecting their finances, such as penning regular updates and blogs on topical issues.

While most advisers have been connecting with clients through video conferencing over the past few months, it’s an ideal time to look at other ways to enhance their experience, such as using a system that enables them to schedule meetings online.

Social media savvy

Whether we like it or not, social media is here to stay. Done well, it can be a powerful tool for your business, helping you raise your profile online and stay connected with existing clients and connections.

In addition, sites like LinkedIn provide a great means to ‘research’ prospects before a meeting. It’s a good example of how social media can be used to enhance your sales technique.

Transparency and honesty

For many, the key issue when engaging with a financial adviser is transparency, particularly when it comes to fees.

In today’s market, it’s essential to be seen as transparent and honest, with a service that justifies the fees being charged. For some, this will mean making an effort to communicate the value of financial advice. Others may decide to add a fees page to their website so it’s clear that there are no hidden charges.

Therapy and counselling

An increasingly important part of the adviser’s role is to be a sounding board for clients, listening to their concerns and tackling any unconscious biases head-on.

Sometimes you will find that the right option is to do nothing, but it’s your job to explain this and advise clients against making knee-jerk reactions that could damage their financial future.

Those advisers who hone and harness these skills will put themselves in the best possible position to thrive in an ever-changing market.

Your Complete Guide To Renewing Your Professional Indemnity Cover

Earlier this year, the Personal Finance Society confirmed it had been contacted byfinancial advisers 'across the country' who have experienced 'significant' hikes in their PIpremiums.

So why is this happening? And what can you do when it comes to renewing your PI cover?

Why Renewing Your PI Insurance Is Becoming More Difficult

Sad as it is to say, in recent years financial advisers have generated more PI insurance claims than most other professions. The industry has found itself at the centre of several high-profile mis-selling scandals and now faces a new threat in the shape of DB pension transfers.

While premiums have steadily been rising in recent years, anecdotal evidence suggests that firms are now seeing their PI insurance bills rise at a previously unprecedented level. Some adviser firms that offer DB transfers have saidthey are struggling to obtain or afford the cover they need, with some quoted a 500% increase in premiums.

There are three main reasons why PI insurers have been spooked:

- The British Steel pension scheme scandal

- In April, the Financial Ombudsman Services' (FOS) limit for complaints about actions by firms on or after that date rose from £150,000 to £350,000

- Supervisory reviews from the FCA. Last year the regulator reviewed 13 firms and judged that fewer than 50% of DB transfer cases were clearly suitable. These concerns were reiterated in an update this summer

The Knock-On Effects In PI Insurance

The factors above, and other issues, have had several knock-on effects on advisers and planners looking to renew their PI insurance:

- Higher premiums - a year ago one trade press reported that PI premiums had risen by 21% in the previous year. Since then, some advisers have seen their premiums increase up to four-fold

- Restrictions - Some PI insurance providers are telling firms that they can only conduct a certain number of pension transfers in any given year

- Higher excesses - another trade press reports that some advisers have seen DB transfer coverage excesses increase tenfold on renewal, from £10,000 to £100,000

- Shorter renewal terms - some insurers are now offering renewals for only 12 months, rather than the previous 18-month period.

While it may seem as if getting the right cover at a fair price is impossible, don't panic.

5 Tips When It's Time To Renew Your PI Insurance Cover

- Prove Your Service

You'll find that it's easier to secure acceptable PI insurance terms if you can evidence that your clients are receiving the level of service and reviews that you have promised.

Keeping excellent records of your service, including review meetings etc. can show an insurer that you're doing what you say you will. If you receive a complaint in the future, you can demonstrate that you did exactly what you said you would - and you can prove it.

- Start The Process Early

Don't leave your PI insurance renewal until the last minute. Think about approaching insurers up to three months before the renewal date of your existing cover.

Starting the process early gives you more time to search the market and to find the right cover for your business.

- Improve Your Submission To PI Insurers

Insurance is all about managing risk. And, your proposal form is a representation of the quality of your business to the insurance market. So, if you can make your submission attractive to an underwriter, you will increase your chances of getting competitive terms.

Ideally, you should supply a written document that outlines your philosophy and sets out the framework within which your business operates.

For example, this could include whether your firm considers requests from existing clients only (which is likely to be a lower-risk position) or accepts wider referrals. This document may also detail your compliance process and who carries this out.

Invest some time in ensuring your submission looks professional. An underwriter will base their assessment on this document (as well as other information online, such as your website) and so if you can submit a quality presentation, you're likely to secure the best terms.

- Shop Around For Cover

Many firms use an insurance broker to secure their cover, with the broker searching the market to find not just the lowest premium, but also the most acceptable terms.

Alternatively, you can head online where you'll be faced with a wide choice of comparison sites and insurers offering terms - however they almost all exclude financial services firms, so using a broker tends to (currently) be the best way to reach the market.

- Consider Joining A Network

If you believe there is a risk that PI insurance cover may not be offered, either now or in the future, you might want to think about joining a network like Beaufort Financial (of course!) to have the security of a larger policy negotiated on your behalf.

If you need any further information, don't hesitate to get in touch. Equally, if you don't agree, I'd still love to hear from you.

Why Marketing Equals Impact

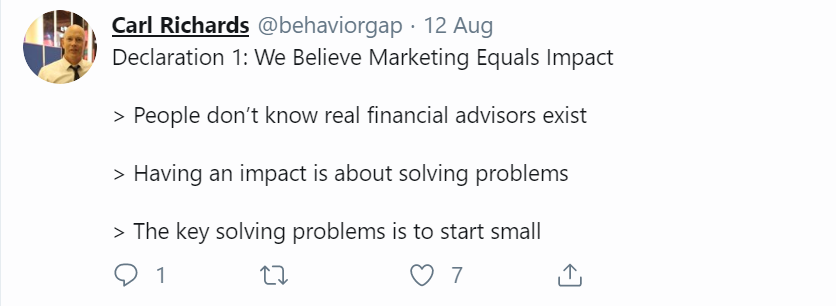

A few days, ago, I noticed this fascinating tweet by Carl Richards. If you don't know Carl, he's a financial planner and creator of Behavior Gap, where he makes complex financial concepts easy to understand.

As part of Carl's manifesto, his first declaration was that 'We Believe Marketing Equals Impact'. It got me thinking about how you create truly impactful marketing, and the impact that good marketing can have on your business.

As Carl says, 'people don't know that real financial advisors exist'. So, how do you use marketing to solve this problem?

You need a strategy

Think about how you deal with your clients. They come to you with a problem or challenge that they are facing. They may even have some idea of how to tackle it. However, by the time they leave you, they have a plan and will understand the importance of thinking more strategically.

It's exactly the same for businesses with a marketing 'problem'. Strategy will help you to:

- Understand your target markets so you know what you should be doing to market your business effectively (see more below)

- Understand your own business, so you know what your key USPs are and where you offer a point of difference. Once you're clear on what your business does, it's easy to explain it to others

- Set out your aims and objectives

- Measure the effectiveness of your current activity

- Focus on the right opportunities for your business, allowing you to target your resources at the right activity (this will save you time and money)

- Understand the ways in which you measure the effectiveness of your marketing strategy.

Know your target clients

Understanding who your target clients are is so important that I'm going to treat it separately here. If you don't understand the people you are marketing to, how will you attract them?

As a start, build up some client personas which should include information such as:

- Age, gender, location, income and employment status

- A summary of the concerns and problems these clients have, and what might trigger their search for advice

- What you can do to help solve these problems and help the clients to achieve their goals

- How these clients make decisions, and what is important to them

- What clients' objections to taking advice might be. Why would they elect not to take advice or choose another adviser?

You'll probably know much of this information from your existing client base. If not, conduct a client survey or focus group to build up a clear idea of who you want to target.

Decide where to focus your marketing resources

Firstly, it's important to remember here that your marketing resource isn't just your spend in pounds and pence. It's also your time in monitoring the effectiveness of your campaign and making changes as appropriate.

For example, getting active on social media might actually not cost you a penny in marketing spend. However, monitoring your account, following like-minded people, scouring the web for great content to share, writing your own blogs and newsletters, and creating enticing images to accompany your posts might take a fair bit of time!

Here's another suggestion: improving your referral process could also help you to generate new leads and new business without you having to spend anything.

If you do have a marketing budget, heading online is a good place to start.

To do that, have a think about how a potential new client finds their way to you. Either they get your name from a friend or colleague or are referred to you. Their next step will probably be to type you into a search engine and see what the results show.

So, at the very minimum, you need to be visible online. Imagine, though, if you could create an amazing first impression. You'd appear high in the search results, with a fully completed Google profile that shows lots of positive reviews and links to your popular social media accounts.

When a potential customer clicks, they would then get to see your website which explains who you are, what you do and why they should choose you. Social proof such as testimonials, award wins and client videos can really help.

Of course, a potential client may be looking to solve a problem but may never have heard of you. That's when your client personas are so important, as you can carefully target potential clients by gender, age, location, and search term using Facebook, LinkedIn and Google AdWords.

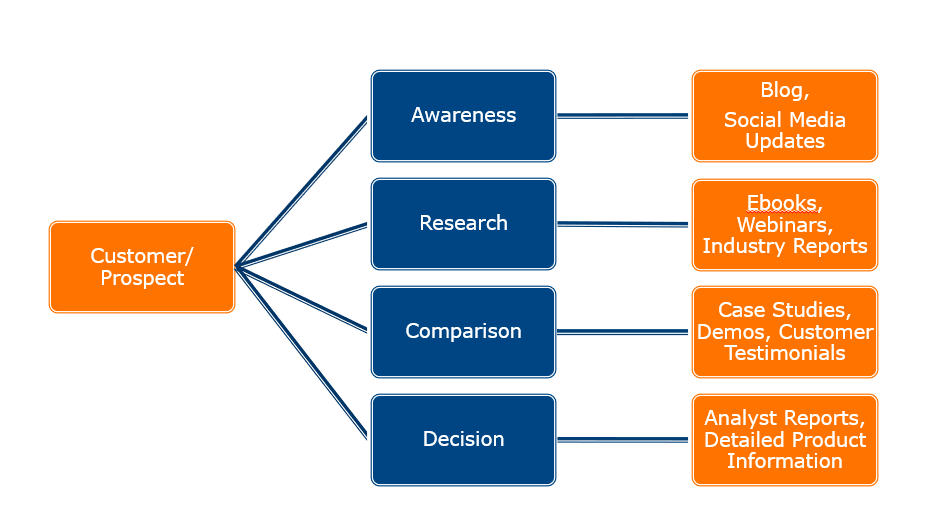

It's about mapping the content to the customer journey:

Measure your success

Often, I hear clients talk about marketing to 'build their brand' or to 'raise their profile'. In theory, these are perfectly laudable objectives - but how on earth will you know when you have met them?

If you're going to implement a marketing strategy, you have got to have goals and you have to be able to measure them. Examples might be:

- 20 new downloads of your pension guide

- 10 completed contact/enquiry forms

- Increasing website traffic by 20%

- Reach 500 Twitter followers

- Increase the number of newsletter sign-ups by 75

Of course, knowing what you want to achieve also helps you to define your marketing plan. Improving your Search Engine Optimisation or using AdWords is likely to get more traffic to your website. Creating useful and shareable content on social media will help you attract more followers.

Whatever you do, make sure you measure it - otherwise, you'll never know what has worked, and what hasn't.

Getting your marketing right

In the past, I've looked at why it's important that you understand the areas in which you add value, and delegate everything else.

According to a Cerulli Quantitative Update, financial advisers spend up to 41% of their time on admin and office management tasks. You will, no doubt, be responsible for tasks which aren't in your main field of expertise, or that you don't enjoy. Examples of such tasks include:

- Compliance

- Case reviews

- Training and competence

- Marketing

- Investment management

While all these tasks are crucial to your business, there might be people better placed to undertake them. That's where we come in. We understand that you sometimes need to delegate your marketing to the experts, and that's why we provide an outsourced solution for all the above.

Regards

Simon Goldthorpe

Executive Chairman, The Beaufort Group

Interest rates rise above 0.5% for the first time in a decade

The Bank of England (BoE) has increased interest rates above 0.5% for the first time since 2009.

Today, the Monetary Policy Committee (MPC) voted unanimously to push up the base rate by 0.25% to 0.75%.

That's not a massive increase; savers aren't going to suddenly start seeing real returns on most of their bank or building society accounts and it won't cause significant pain to most mortgage holders.

However, coupled with the 0.25% increase in November last year, it is another warning shot that interest rates aren't going to stay at record lows forever and that those with debt should prepare for further increases.

So, how will today's rise affect you?

If you are a saver

You will hopefully see the increase passed on in the form of higher interest rates.

Nevertheless, it's probably too soon to get over excited. With inflation (as measured by the Consumer Prices Index) currently at 2.3%, you would currently have to tie up your savings for at least five years to get a 'real', above-inflation return. However, tying up capital for that amount of time isn't without risk and is something to think carefully about doing, before making a commitment.

However, we expect savers will welcome any increase in interest rates with a small cheer, even if they aren't breaking out the bunting just yet!

If you are a borrower

How you're affected by a base rate rise will depend on how you are borrowing money.

If you have a tracker mortgage, where the interest rate is pegged to the BoE base rate you can expect your monthly mortgage payment to rise almost immediately. The same is almost certainly true if your mortgage is arranged on your lender's Standard Variable Rate (SVR). If you have a fixed-rate mortgage, you won't see any immediate change to your monthly payments, because as the name implies, your interest rate is fixed and won't change for the duration of the product you selected when you took the mortgage out. However, the pain may only be delayed until your fixed rate ends, at which point your payments may rise due to the increase in interest rates which occurred during the period of your fixed rate.

Whether you are immediately affected or won't be until the end of your fixed rate, all mortgage borrowers should start to prepare for further interest rate rises.

There are three key things to do here:

Check your mortgage deal: Use comparison tools or ask your financial adviser or planner to help you to work out whether you are currently receiving the most competitive rates available on the market. This may mean considering a fixed rate, which will protect you from further interest rate rises for a period.

Review your household expenditure: This will help you to understand whether there are any items you can cut back on to create surplus income which could be allocated to higher mortgage payments should rates rise again. Then, you can begin to benefit from making those cutbacks straight away, potentially using the extra income for your emergency fund.

Build and maintain your emergency fund: If you don't already have one in place, now is the time to take steps to build up an emergency fund. This could help you to recover as and when further interest rate rises take effect, or, as the name suggests, bail you out in a financial emergency.

Should we expect further rate rises?

The BoE Governor, Mark Carney, signalled that three further rate rises will be needed to avoid the rate of inflation remaining above 2% over the next three years.

The report released following the announcement clarifies this: "The Committee also judges that, were the economy to continue to develop broadly in line with its Inflation Report projections, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to the 2 per cent target at a conventional horizon.

"Any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent."

Communicating the benefits of advice: Why there's still more to do

In my experience, most advisers and planners communicate, and demonstrate, the value of advice very effectively in their one-to-one client interactions.

In my experience, most advisers and planners communicate, and demonstrate, the value of advice very effectively in their one-to-one client interactions.

Furthermore, we all know that high-quality financial planning adds far more value to the client than the fees they pay. Indeed, there are times, particularly as people move from the world of work to one of retirement, when financial planning is genuinely life changing.

However, research from YouGov*, commissioned by Beaufort Financial to coincide with the third anniversary of Pension Freedoms, has shown that the wider public awareness of the value of advice is lower than we might have hoped.

Only one in 3 expect to seek advice

The introduction of Pension Freedoms (more of that in a moment), coupled with heightened interest in Defined Benefit and Final Salary pensions, mean that most advisers and planners I speak to are incredibly busy.

Despite that, our survey found that the 'value of advice' message isn't getting through to most people; only 32.08% of the over 50s who have not yet retired expect to seek financial advice about their retirement in the future.

Unsurprisingly, the likelihood of taking advice increases as people get closer to more traditional retirement ages. Even so, millions will retire without seeking any form of financial advice.

Perhaps the lure of early retirement might convince more people to seek advice? Sadly not. Only one in 10 (11.97%) of people who had not already retired, said they were more likely to seek financial advice if it meant they could retire early.

Millions in the dark?

Pension Freedoms represent the single largest change to retirement planning during my financial services career. Used correctly they can help people retire more flexibly, moulding an income to their lifestyle and potentially leaving a financial legacy when they are gone.

Conversely, there's no doubt Pension Freedoms also present a threat if poorly thought through decisions are made.

Pleasingly, among 50-64-year olds 63.84% of people are aware of the rules. However, that leaves approximately 4.5 million** adults potentially in the dark about Pension Freedoms; if they don't know about them, how do they take advantage of the opportunities and avoid the threats?

Gender gap

At a time when many companies are reporting large gender pay gaps, our research revealed that women are 24.91% less likely to take financial advice about retirement than men.

Equally worryingly, significantly more women (50.76%) are unaware of Pension Freedoms compared to men (30.25%). While 60.35% of men are aware that Pension Freedoms could help them retire early, compared to just 39.23% of women.

Where next?

The natural temptation would be to focus on the here and now. After all, most advisers and planners are incredibly busy advising clients and developing their business.

In my view, that would be a mistake.

Why?

Two reasons. Firstly, there's a huge need for advice, eloquently demonstrated by the FCA's 2017 Financial Lives survey, which found that:

- 53% have not reviewed how much their pension pots are worth in the last 12 months: Advice will help these people understand what their pension is worth and more importantly, whether it will provide the retirement they want, and if not, what they can do about it.

- Seven out of 10 (71%) of UK adults with a Defined Contribution scheme were not aware of any charges on their pension: Excessive charges eat into the future income retirees can expect. It often takes an adviser or planner to make clients aware of what they are paying and the effect it will have on their retirement income.

- 17% of consumers who have accessed a pension pot report fully withdrawing their pension pot in the last two years: An adviser will help their clients withdraw money tax-efficiently, taking only what is necessary to meet their needs and helping avoid emotionally driven decisions.

Secondly, when I finally put my feet up and look back on my career, I want to feel that I have contributed to building an enduring and sustainable profession.

I hope you feel the same.

To do that we need to engage with the people who don't plan to take advice. Sure, it will look different:

- More advice will be delivered through the workplace

- Guidance may become more common

- We'll need to innovate to develop propositions attractive to Generations X and Y

However, the prize is worth it. Not only will we create opportunity for those who chose to make financial services their profession, but ensure future generations build a more secure financial future.

I firmly believe the profession I love, and am proud to be a member of, is up to the task.

Finding the right fit; looking for the right DFM

Discretionary fund managers (DFMs) now play an important part in advice firms' propositions. Click here to read the New Model Adviser Outsourcing Roundtable supplement, in association with Beaufort Investment.

Six things you need to grow your financial planning practice

Can you write a piece about business development? they said.

Sure, no problem.

If you could focus on the most important things you need to grow a financial planning business that would be great they said.

Hmm‚

That's not as easy as it sounds.

As the saying goes; there's more than one way to skin a cat, despite that we seem to live in an era where gurus and 'experts' insist there's only one way to accomplish your aim; theirs. Consequently, I'm instinctively nervous about telling experienced professionals how to build a successful practice.

What's more, how does one define success?

For some it could be a purely monetary measurement; the bottom line, a level of assets under management or the margin your business is making. For others it might be a more nebulous but nevertheless important concept, such as work / life balance.

That said, my years have taught me that there are several key components. If all, or most, are in place, you will increase the chances of your business being successful:

1.Define success

We all want different things from our business; there's no right or wrong answer, just what's right for you and those close to you; both personally and professionally.

Nevertheless, it is essential to define what success looks like. Everything else, strategy, tactics and the motivation to continue when times are tough, flows from there.

2.Agree a strategy

Strategy doesn't necessarily have to be complicated; it might just be a series of steps to take you toward a goal. Yet without that strategy in place, the chances of you achieving your desired outcome is significantly diminished. To put it another way: success (however you define it) won't happen by accident.

3.Know your numbers

We all remember the SMART acronym. However, it's not only the end goal that should be measurable. The steps along the way must be too.

For example, if your goal is to take on 10 new clients in the next 12 months, as a minimum you need to know:

- The type of clients you want to attract; you can then measure the enquiries you receive against the 'ideal' client

- Your conversion rate; allowing you to understand the number of new enquiries needed to retain the 10 clients

- The current number of enquiries you are receiving; which will tell you whether you are already receiving sufficient new enquiry numbers, or you need to increase your marketing efforts

- Finally, the number of new clients retained

While the last number represents the headline goal, each element represents an essential component and therefore should be reported against.

4.Get the right people around you

If I've learnt one thing over the years, it's the importance of having the right team around me.

Finding those people is only part of the job though. You must invest in them. That might mean giving them your time or arranging specific training. It also means empowering every member and trusting them to get on with the job.

Let go and let others get on with their job, so you can get on with yours.

5.Get your marketing right

If you don't have clients you don't have a business.

Obvious, yes.

Harsh, perhaps.

True, certainly.

I've often wondered what separates the most financially successful advisory firms from the rest.

There's a long list of factors, however I'd place the ability to generate new clients right at the top of that list. If you don't have that ability, or can't outsource it, the likelihood of hitting your goals will be significantly reduced.

6.Persistence

In the list of factors separating those who achieve success and those who don't, persistence is key.

The ability to continue working towards your goal, in the face of everything life throws at you, is usually the difference between success and failure.

As Winston Churchill said: "Success is not final, failure is not fatal. It is the courage to continue that counts." In other words, as he was also apparently fond of saying, it's the ability to keep buggering on which really counts.

It's not for me to tell you how to be successful, or even how to define it. However, in my experience, it's these six things which increase the chances of your success; whatever that means for you.