Your guide to writing a will

November marks Will Aid Month. We want to take the opportunity to remind you just how important a will is and explain why it should be considered a crucial part of your financial planning.

You no doubt have an idea of what you'd like to happen to your wealth and assets once you pass away. For many, it will mean leaving it to children or grandchildren. But you might also want to leave something for other family members, friends or charity. A will is crucial for ensuring your wishes are carried out.

Should you die without a will in place, your assets will be distributed according to the Rules of Intestacy. These specify a rigid order of who should benefit from your estate. It's unlikely that these will align with exactly what you want. This is particularly true for modern, often complex, families.

If, for example, you have children from a previous relationship, have since remarried and the value of your estate is worth less than £250,000, all your wealth will pass to your surviving partner. This could effectively disinherit your children.

Despite the importance of a will, it's a step that many in the UK are failing to take. More than half (56%) of parents in the UK with children under 18 have no will, a survey by Will Aid revealed.

Writing a will should be a task you undertake in the context of financial planning too. With the right information, you can understand what inheritance you can leave behind. This allows you to decide how you want different assets distributing.

Thinking about your legacy with wider financial goals in mind can help give you confidence and improve financial security too. Perhaps you're worried about spending too much during your retirement years for fear of not leaving the legacy you want behind. Financial planning can give you an understanding of how lifestyle changes will affect what you leave to loved ones.

With this in mind, these are the steps you should be taking as you prepare and write your will:

1. Value your estate

It's hard to think about the distribution of assets if you don't know the value of them. A good starting point for writing your will is creating an up-to-date list of what your assets are and how much they're worth. This is an area we, as financial professionals, can help you with, as well as providing an insight into how the value might change over the years depending on your retirement decisions.

2. Deciding on beneficiaries and distribution

Next, you should spend some time thinking about who you'd like to inherit your wealth. It's likely there's more than one person you want to leave an inheritance to. Once you have a list of beneficiaries, you'll need to consider how you want your estate to be distributed.

You should be as specific as possible here. While you can allocate each person a portion of your estate, it may be a complicated process to distribute your estate depending on your assets. For example, if three children equally inherit a property, they'll have to come to an agreement as to how they'll proceed. Perhaps you have some jewellery you'd like to go to your granddaughter or a property that will suit a son with a growing family. If you have a specific request for items or assets, make it clear.

3. Assess Inheritance Tax liability

Do you know if your estate will be liable for Inheritance Tax (IHT)? If your estate's value is more than the Nil-Rate Band and Residence Nil-Rate Band for IHT, it may change how you use and distribute your wealth now.

The current Nil-Rate Band is £325,000. If your estate is worth less than this, no IHT will be due. If you're passing on your main home to children or grandchildren, you may also be able to take advantage of the Residence Nil-Rate Band. This is currently set at £125,000, rising to £175,000 in 2020/21.

There are several steps you can take to reduce IHT liability or help your loved ones cover the bill they may face. If you'd like to understand what IHT may be due when you pass away, please contact us.

4. Consider a charitable donation

Many people choose to leave a charitable donation as part of their legacy. If you've been a lifelong supporter of a cause, naming charities in your will can be an excellent way to continue this. As with all beneficiaries, you should be as specific as possible about what you want a charity to receive from your estate.

Leaving a charitable donation can have IHT benefits too. Leaving 10% or more of your estate to charities means your IHT rate will be decreased from 40% to 36% if your estate is liable.

5. Note other wishes

While the main aim of a will is to ensure your estate is distributed in line with your wishes, it can also be used to cover other areas.

If you have dependents, for example, you can name a guardian to care for your children until they're 18, as well as someone to look after their inheritance. You may also choose to make your preferred funeral arrangements known, though this would not be legally binding.

6. Choose executors

Executors are the people who deal with distributing your estate. It's a good idea to choose more than one executor; you can appoint up to four and those chosen can also inherit from your will.

An executor should be someone you trust and who is able to take on the responsibility of the role. It can be a friend or family member. Alternatively, you can appoint a professional executor, such as a solicitor or an accountant. A professional executor will take their fee from your estate and they can be a good choice if your estate is complex.

7. Writing the will

With your legacy plans set out, it's time to write your will. There are several options when doing this.

You can choose to make your own will, but you should keep in mind it's a legal document that needs to be written and signed correctly to be valid. Often, taking advice from a regulated solicitor that specialises in wills and probate is the best course of action.

Whichever option you choose, make sure your will is valid. Your will must be in writing, signed by you and witnessed by two people. Beneficiaries should not act as witnesses, and, where possible, neither should executors.

8. Storing and updating

Once you've written your will, there are two points to remember. The first is to store it in a safe place, this could be in your home, with a solicitor, bank, or a Probate Service, and ensure your executors know where it's kept.

Secondly, don't write a will and forget about it. Circumstances can change considerably; your wishes today can be very different to those you will have in a decade. It's good practice to review your will every five years and after big life events, such as getting divorced, receiving an inheritance or having children.

While you're writing your will, there is another task you should tick off; naming a Lasting Power of Attorney (LPA).

An LPA gives someone you trust the power to make decisions on your behalf should you become too ill to do so. An LPA can only be written while you're sound of mind. As a result, it's an important step to take before it needs to be used. The combination of a will and LPA can help make sure that your wishes are carried out through your later years of retirement and once you pass away.

To discuss your finances and the legacy you leave loved ones, please contact us today. We can help you put the figures in context with your wider aspirations.

Autumn Budget 2018: Were you a winner or a loser?

Will you be better or worse off because of today's Budget?

In a relatively quiet Budget our summary answers that question, please read on to find out.

Winners

Earners

The Chancellor brought forward an election pledge to increase both the Personal Allowance and Higher Rate tax band, affecting 32 million people. From April 2019, the Personal Allowance will increase to £12,500, while the higher rate tax threshold will be £50,000, rising from £11,850 and £46,351 respectively.

The National Living Wage will also increase to £8.21 from April 2019 from the current £7.83, representing a 4.9%, and significantly above inflation, increase.

Homeowners

Main residences will remain exempt from Capital Gains Tax (CGT), ensuring families that sell their home don't face a tax from the sale of their property.

Furthermore, all shared equity purchases of up to £500,000 will be exempt from Stamp Duty.

Small businesses and self-employed

The threshold for VAT registration will remain unchanged for the next two years despite speculation that it would drop. The fact the current £85,000 turnover threshold remains in place will be a relief to many people who are self-employed or run small businesses.

Businesses occupying property with a rateable value of less than £51,000 will have their business rate cut by a third over the next two years. The amount businesses pay in rates has been a longstanding issue for many, particularly those in retail as the high street attempts to compete with online businesses. The changes will mean savings for 90% of shops, restaurants and cafes.

Finally, a £695 million initiative that will help small businesses to hire apprentices was also announced. Those firms taking on apprentices will have the amount they need to pay halved.

People paying into pensions

Despite concerns ahead of the Budget that there would be some changes to tax relief on pensions, no changes were announced in the speech. For those paying into a pension, it provides some level of certainty, at least for a further year.

Losers

Technology giants

There will be a new tax targeting digital businesses. The UK Digital Services Tax will target specific platform models and technology giants. It will only be paid by firms that generate £500 million in revenue globally and will come into effect in April 2020. Digital tech giants will be taxed 2% on the money they make from UK users.

Tax avoiding businesses

Once again, the Chancellor accounted that there would be a clampdown on large companies that avoid paying the correct level of tax. The Chancellor aims to raise £2 billion over the next five years by targeting tax avoidance and evasion.

Questions?

If you want to discuss how you are affected by today's Budget or have any questions, please contact us to speak to one of our finance professionals.

The content of this newsletter has been provided by The Yardstick Agency and is based upon their interpretations of today's Budget. Further analysis and clarifications will be published as necessary.

Autumn Budget 2018: Everything you need to know

Just after 3.30 pm today the Chancellor, Philip Hammond, stood up to deliver the first Budget on a Monday since 1962 and the last before Brexit.

He started by saying this would be a Budget for "hard-working families … who live their lives far from this place ... and care little for the twists and turns of Westminster politics".

Nevertheless, he soon turned to Brexit although, as usual, he started with a review of the state of the UK economy.

The economy and public finances

The Chancellor said growth would be resilient and improve next year from an Office for Budget Responsibility (OBR) forecast of 1.3% to 1.6% in 2019, then 1.4% in 2020 and 2021, 1.5% in 2022 and 1.6% in 2023.

He also reported that the OBR predicts real wage growth in each of the next five years.

Turning to borrowing Mr Hammond reported that it will be £11.6 billion lower than forecast earlier this year. He then said it would fall from £31.8 billion in 2019/20 to £26.7 billion in 2020/21, £23.8 billion in 2021/22, £20.8 billion in 2022/23 and £19.8 billion in 2023/24, which would be its lowest level for more than two decades.

Brexit

The Chancellor said we are at a pivotal moment in the Brexit talks with a deal leading to a potential double Brexit dividend.

However, he also went on to say that amount spent on 'no deal' planning will be increased to £2 billion. He also made it clear that the Spring statement might be updated to a full Budget, depending on the Brexit outcome.

Alcohol, tobacco and fuel

It was announced in October that fuel duty will be frozen for the ninth consecutive year.

Tobacco duty will rise by an amount equal to inflation plus 2%. However, beer, cider (except white cider) and spirits duty will be frozen for a year. Duty on wine will rise in line with inflation.

Living Wage

Mr Hammond announced that the National Living Wage will be increased, rising from 4.9% from £7.83 to £8.21 from April 2019. He said this would benefit around 2.4 million workers.

Tax

The Chancellor bought forward a manifesto commitment announcing that from April 2019 the Personal Allowance (the amount you can earn before you start to pay tax) will be raised to £12,500 and the higher-rate threshold to £50,000.

He said this was equivalent to £130 in the pocket of a basic rate taxpayer.

He also reconfirmed his commitment to an individual's main residence remaining exempt from Capital Gains Tax (CGT). However, he announced a reduction from 18 to nine months in the period a home continues to qualify for CGT relief once the owner has moved out.

VAT

In a relief for many small business owners, the Chancellor announced that VAT threshold will remain unchanged for the next two years.

Universal Credit

The Chancellor announced a further £1 billion over five years to help with the transition as existing welfare claimants move to Universal Credit.

Housing

Mr Hammond announced that the number of first-time buyers was at an 11-year high.

He went on to confirm that the Stamp Duty exemption announced in the 2017 Budget would be extended to first time buyers who buy shared ownership properties. This change will be backdated to first-time buyers who purchased a share ownership property after the last Budget.

No other changes to Stamp Duty were announced.

He also announced a further £500 million for the Housing Infrastructure Fund to support the building of 650,000 new homes.

Pensions & ISAs (Individual Savings Accounts)

Despite the usual pre-Budget speculation, the Chancellor made no mention of pensions in the Budget.

There had also been some people who suggested the Chancellor would make changes to Lifetime ISAs (Individual Savings Accounts). However, nothing was mentioned in his speech about Lifetime ISAs, or indeed any other type of ISA.

However, it has subsequently been confirmed that the maximum annual ISA subscription will remain unchanged at £20,000.

Premium Bonds

While not in the speech, it has been revealed that the minimum investment for Premium Bonds will be reduced to £25 from £100.

Furthermore, other people not just parents and grandparents will be able to purchase Premium Bonds for children under 16.

Business

The Chancellor said a package of measures would show that Britain is open for business.

The most headline-grabbing of these was perhaps a new Digital Services Tax targeting established tech giants. Mr Hammond was keen to point out this would not be an online sales tax stating it would only be paid by profitable companies with a worldwide turnover of at £500 million.

Starting in 2020 he said it would be expected to raise over £400 million per year.

Turning to smaller businesses, the Chancellor announced that business rates for businesses occupying commercial properties with a rateable value of £51,000 or less will be cut by a third over two years.

He also announced a new £695 million initiative to help small firms hire apprentices with the amount they pay being cut by 50%.

Finally, he announced a £650 million package to help ailing high streets.

Health and education (England only)

The Chancellor confirmed the injection of capital into the NHS announced by the Prime Minister earlier this year describing it as a £20.5 billion real terms increase for the NHS.

He also announced at least £2 billion per year, by 2023/24, of extra funding for a new mental health crisis service.

At the same time, he announced a one-off £400 million for schools to help them pay for the little extras they need. Mr Hammond said that would be the equivalent of £10,000 for every primary school and £50,000 per secondary school.

Plastic tax

Finally, a new tax on packaging which contains less than 30% recyclable plastic was announced. Although the Chancellor resisted the temptation to impose a direct tax on single-use plastic cups.

Questions?

If you have any questions about the Budget and how it might affect you please do not hesitate to get in touch.

The content of this newsletter has been provided by The Yardstick Agency and is based upon their interpretations of today's Budget. Further analysis and clarifications will be published as necessary.

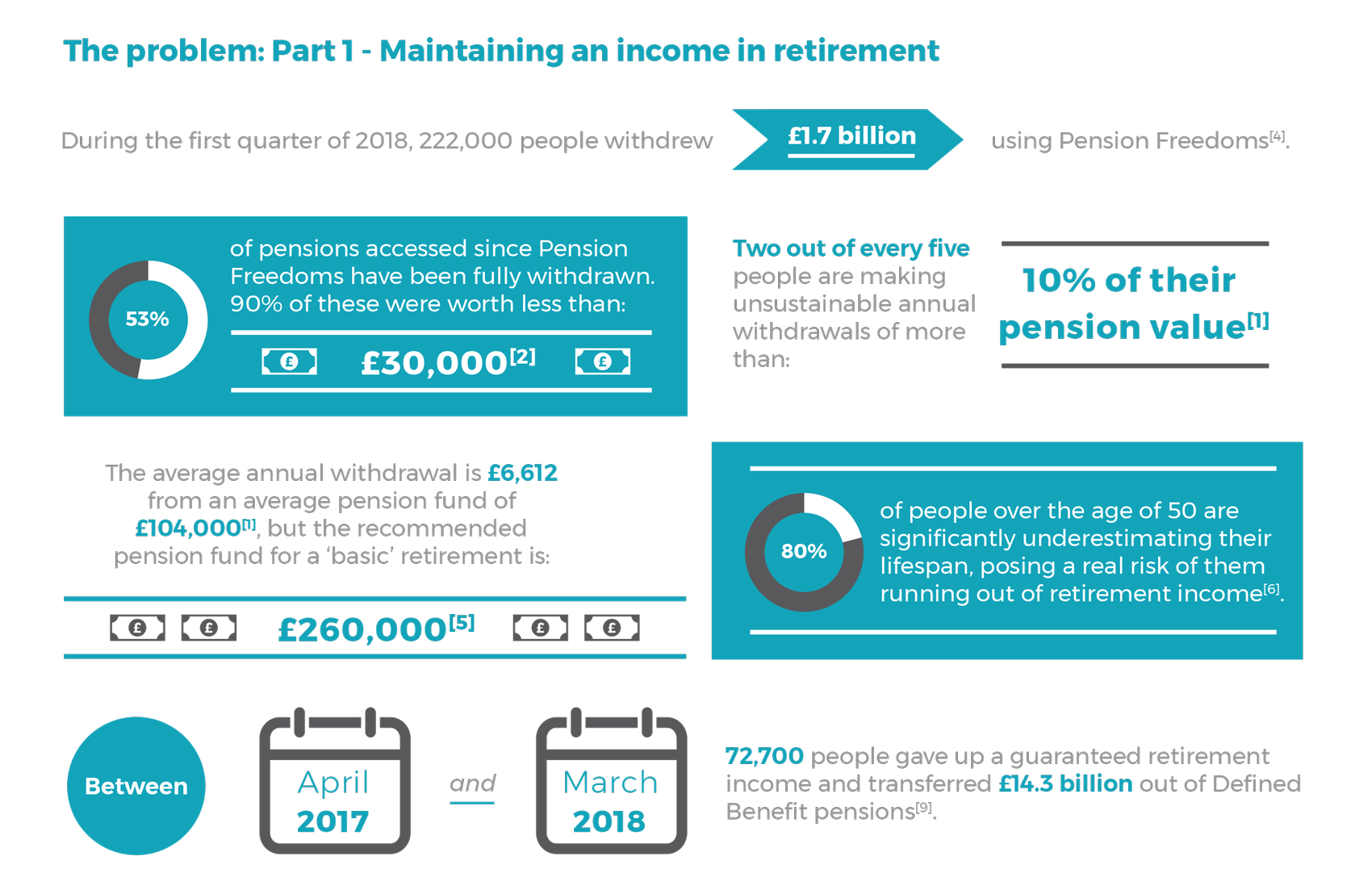

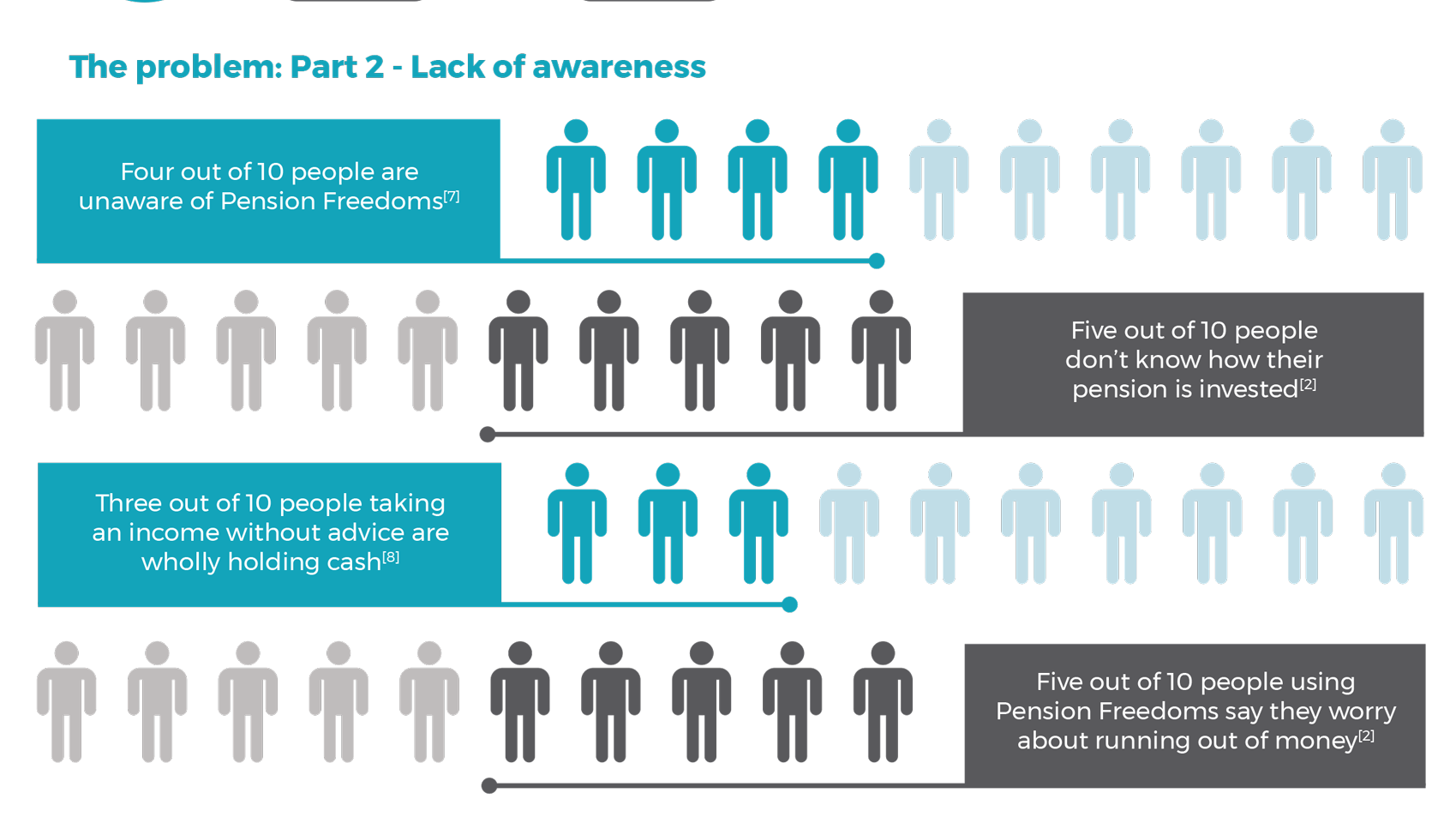

Focus On: Pensions Freedom Seminar

On the 27th September we held our very first 'Focus On' seminar.

Primarily for solicitors and accountants, we took a look at two key problems that have come to the fore since the introduction of the new pension freedom rules in April 2015, and some solutions the we believe can help solve the problems.

Sources: (1) AJBell (2) AJBell (3) Schroders (4) Gov.UK (5) Royal London (6) Retirement Advantage (7) Beaufort Financial/YouGOV (8) FCA (9) The Pensions Regulator

We believe part one of the solution is an educational one, and by highlighting and explaining key things to know, we hope our attendees are now better informed to guide their clients.

To support and compliment the educational piece is our six step planning solution. Here it is in brief:

We received some excellent feedback from those who attended. We work with solicitors and accountants on a regular basis, so if you ever need legal or tax advice, please do ask us, as we are likely to know someone who can help you.

Have you considered the cost of care in retirement?

In the next 20 years, the number of elderly people needing constant care is expected to double. You've probably thought about how long your pension needs to last and whether you're saving enough. But have you factored in the cost of care?

By 2035, it's expected there will be 446,000 adults aged over 85 that need 24-hour care, according to research from Newcastle University. It's a similar picture for those aged over 65 too; it's thought one million will need constant care. The figure represents an increase in demand by more than a third.

It's a figure that's partly driven by a growing population. However, longer life expectancy is playing a role too. Estimates show:

- The number of people aged over 65 will increase by almost 50% in the next 20 years; reaching 14.5 million in 2035

- Life expectancy will increase by three and a half years for men and three years for women

Typically, retirees spend more in the early years of retirement. The first years after giving up work are often marked by a greater level of spending, such as paying off the mortgage or travelling. As people settle into retirement, costs often decrease. Care changes this.

The cost of care varies depending on where you live in the UK. However, the average annual cost of a care home is around £29,270, according to PayingForCare. This rises to £39,300 if nursing is required.

Even if you don't require constant care, it's likely you'll need some level of support at home. If this can't come from loved ones, you could be looking at a cost of £15 per hour. At first glance, that doesn't seem like a big expense. But when you calculate that two hours of help a day will amount to £10,950 a year, it's clear that most people will need to plan ahead for this.

With these sums in mind, it's important to factor the cost of care when planning your pension income.

Making care part of your retirement planning

Nobody wants to think about needing care as they age. But considering what you would like and how you would pay for it can make seeking care easier and less stressful should you ever need to.

Spending in retirement follows a similar pattern for many. When you first enter retirement you're likely to find your essential outgoings are reduced but that your spending on luxuries will increase. It's common to want to enjoy those first years of retirement, whether you plan a few more holidays or increase social activities now you're no longer working.

It's then typical for your spending to settle and perhaps decrease as you enter the next stage of retirement before outgoings increase again as you start paying for care. The differing income needs throughout retirement can make it difficult to ensure your pension lasts throughout your later years.

Considering what you would choose should the need for care arise can help you forecast costs. Among the questions to answer are:

- Do you have any medical conditions that may affect your ability to care for yourself?

- Are your loved ones in a position to offer you support if needed?

- Would your current home be suitable if you were to experience reduced mobility?

- What type of care would you prefer?

- Is there a way to protect some of your assets when paying for care?

Of course, no one can predict what will happen in the future. But having an idea of what level of care may be required and the expenses associated can help you create a realistic financial plan. It's also a good idea to speak to your family about what your preferences would be and how it would be paid for. They may have alternative suggestions, such as how they can provide support, and it could affect their inheritance.

Appointing a Power of Attorney

While we're on the subject of your financial health and care, there's another area where it's important to be proactive; appointing a Power of Attorney.

A Lasting Power of Attorney (LPA) is a legal document that appoints one or more people to make decisions on your behalf. Should you have an accident or illness that means you can't make your own decisions, those appointed will be able to make them for you.

There are two types of LPA, both are important. A health and welfare LPA will make decisions relating to areas such as medical care, moving into a care home, and treatment. A property and financial affairs LPA will allow your loved ones to manage areas such as your bank account, paying bills and selling your home.

It's a common misconception that your partner will be able to take control of your finances. Even if you have a joint account, they may not automatically have access to it. This is because a joint account can only be operated with the agreement of both parties. As a result, appointing an LPA is important, no matter your personal circumstances.

If you'd like to understand how the cost of care could affect your retirement plans or whether your pension would cover the care required, you can contact us today. We'll help you understand what steps you should be taking and how it will affect your income.

Tips for planning for your future if you're part of the 'Sandwich Generation'

If you feel as though your finances are under pressure as you support both children and elderly parents, you're likely to be part of the 'Sandwich Generation'. Research has found that many of those aged between 40 and 60 are struggling with financial responsibilities.

Despite being caught in the middle of two types of dependents, many in the Sandwich Generation aren't financially prepared, according to a survey from LV=.

Among those dubbed the Sandwich Generation:

- 52% are worried about the consequences of a serious illness affecting themselves or their partner

- 30% are worried about the prospect of themselves or their partner dying and leaving the family without an income

- 54% want to save but can't afford to

- 37% have less than £125 disposable income each month

- 46% cite children as a constant source of unexpected expenses

While working to support families, the Sandwich Generation is neglecting their own long-term financial security. On average those within this group have a pension valued at £60,000 that they expect to last 20 years. It's an amount that is likely to result in an income of less than £260 a month, according to LV=. Even when the full State Pension is added, assuming you qualify, at £164.35 per week, many are facing a retirement struggling financially.

Justin Harper, Head of Marketing at LV=, said: It's clear this group feel they are being pulled in many directions, with pressures to care for older relatives and ongoing responsibilities for their children. The Sandwich Generation have huge financial obligations and with the rising cost of living, are worrying about what could be around the corner. Spreading finances too thinly and dwelling on their worries, means the impact of having little to no plans in place, could expose them to a real income shock.

Five tips if you're part of the Sandwich Generation

With different priorities pulling at your finances, it can be challenging to manage daily expenses alongside building security. These five tips can help get you on the right track:

1. Create a realistic budget

Setting out a monthly budget that covers everything, from utility bills to savings, can help you find the areas to cut back on.

You probably already have some sort of budget, even if it's just in your head. But writing it down and keeping track of what you're spending makes it far easier to stick to. If you find you're regularly going over what you set aside to spend or undersaving, you may need to revisit what's realistic.

Of course, there are times when unexpected bills crop up. Leaving a portion of your income to act as a buffer in these events can help.

2. Build up an emergency fund

The Money Advice Service (MAS) recommends having a safety net of at least three months' salary to fall back on. However, 57% of the Sandwich Generation don't have this amount, the research found. As a result, 34% don't feel they could handle a personal financial crisis.

If you're among those that don't have an emergency fund, now is the time to build one up. Looking at the end figure can seem daunting. Instead, focus on putting away a small portion of your wage every month as soon as you're paid. Breaking it down into smaller chunks can make creating a financial safety net more manageable.

When your finances are really under pressure, even putting away small sums can seem impossible. But making it part of your monthly budget can mean you feel far less apprehensive about the future.

3. Consider protection

If you're one of those that are worried about how your family would cope should something happen to your income, some form of protection can give you peace of mind.

Income Protection that will pay out monthly in the event of illness or injury, for example, can ensure both you and your loved ones have a safeguard in place. There are other options too, such as Critical Illness Cover and Life Insurance. Which one is right for you will depend on your situation and what you're concerned about.

When your finances are already stretched, it can seem like an unnecessary expense. However, consider the financial consequences of not having any cover should illness, injury or death strike.

4. Don't neglect your own financial future

With a focus on providing for ageing relatives and children, the research suggests the Sandwich Generation are doing so at their own expense. Don't forget to take steps to secure your own financial future too.

One of the key steps to take here is to save into a pension. If you're working full-time, you've probably been automatically enrolled into a Workplace Pension in the last couple of years. While you can opt out of this, it's short-sighted.

5. Talk to a finance professional

There's a common misconception that financial advice is only for the wealthy. The truth is that it can help you to get the most out of your money. Seeking the advice of a financial adviser or planner can help you balance the needs of today with those in the future.

By better understanding how your money choices will affect your financial security immediately and in the future, you'll be in a better position after speaking to a professional. Contact us today to get the process started.

Sustainable investment continues to grow: Do ethics affect your investment choices?

Investors are increasingly investing their money with sustainability concerns in mind, figures show. As October marks Good Money Week, we take a closer look at what ethical investing is and how the market's growing.

It's predicted that the UK's ethical investment market will grow by 173% by 2027, according to research from Triodos Bank. With the projected total amounting to £48 billion, ethical investing is slowly moving into the mainstream. But what is it and how does it influence your investment choices?

What is ethical investment?

In simple terms, ethical investing is where you invest your money with other considerations beyond the financial return in mind. You base your investment decisions on the impact your money could have; creating a double bottom line if you will.

When you look at changes in society in general, it's not surprising that ethical investment is growing. Have you already cut down on the amount of plastic you use? Do you purchase Fair Trade items from the supermarket? Or are there some brands you avoid because they test on animals? These are ethical decisions you make as part of your daily routine; ethical investment is an extension of this.

Ethical investment comes in many different forms and there are a lot of terms used to broadly cover the same motives. You may have heard phrases like sustainable investment, responsible investment, SRI (socially responsible investment) or impact investing. ESG (environmental, social and governance) is another commonly used term that breaks down ethical investing into three core areas of consideration:

Environmental: These are investment concerns that cover a range of environmental impacts. Companies developing renewable energy sources, providing alternatives to deforestation or taking steps to improve the local ecosystem can fall into this category in a positive way.

Social: Again, the social segment covers a broad range of issues. Providing safe working environments, paying a living wage and ensuring no children are employed throughout a supply chain, are social issues to consider. It can also cover a company's impact on the communities where it operates.

Governance: Governance issues focus on how the company is run. Funds that cover governance issues may, for example, look at female representation on boards, whether the company avoids paying taxes or remuneration levels of the highest paid executives.

What's the size of the ethical investment market?

When you look at the size of the whole investment market, the number of funds taking ESG factors into consideration is still niche. However, it is growing, and the pace of growth is set to increase.

In 2023, the market will reach a 'tipping point', according to Triodos Bank. This is partly being driven by the next generation of socially conscious investors seeing an increase in their income. As a result, the UK market alone is expected to reach £48 billion by 2027.

The Triodos Bank research found:

- 55% would like their money to support companies which contribute to making a more positive society and sustainable environment

- 61% of investors believe that for the economy to succeed in the long term, investors need to support progressive businesses tackling ESG issues

- A fifth of investors are planning to invest in an SRI fund by 2027

- Ethical investment appeals more to younger generations; 47% of those aged between 18-34 intend to invest in an SRI fund within the next nine years

- Within this group, 56% are motivated to invest in ethical funds because of climate-related disasters in the news; compared to 30% for older counterparts

While there is a growing interest in ethical investment, there is still a limited market, which can make it challenging. 73% of UK investors have never been offered ethical investment opportunities. Furthermore, 61% would not know where to go for more information in SRI.

Despite this there is a demand for more information; 69% of investors would like to have more knowledge and transparency about where their money goes.

The challenge of defining 'ethical'

You may have already spotted one of the biggest challenges with ESG investing; we all have different values and ethics. It's a highly subjective area.

You may consider a company to be ethical because it's taking proactive steps to improve the lives of its employees in the poorest parts of the world. Someone else, on the other hand, may say the company unethical because the firm operates in the oil and gas sector, resulting in environmental degradation. As a result, it's important to define what your personal priorities are, as well as where you're willing to compromise, before you start looking at ethical investment opportunities.

According to Triodos Bank, these are the five biggest issues that would put off investors:

- Manufacturing or selling of arms and weapons (38%)

- Worker/supply chain exploitation (37%)

- Environmental negligence (36%)

- Tobacco (30%)

- Gambling (29%)

So, how do you invest with your values in mind? There are three key ways to do so:

Negative screening: This is where you actively remove companies from your portfolio or avoid investing in them because you don't consider them to be ethical.

Positive screening: Positive screening is where you actively invest in companies that align with your principles, allocating a portion of your investable assets to support these firms.

Engagement: An engagement strategy is where you use your power as a shareholder to promote long term, ethical changes. As it relies on shareholder power, it's a strategy that's more effective for institutional investors, such as pension funds, than the average retail investor.

The above are ways of investing ethically and striving to encourage change but do this in very different ways. In the case of energy and reducing the amount of carbon emissions, for example:

- A negative screening approach would divest from oil and gas companies

- An investor using positive screening would put their money into renewable firms

- While those using the engagement approach would hold shares in oil and gas but vote at Annual General Meetings to invest in sustainable technologies

As with all investments, you do need to balance the risk of your investments potentially decreasing in value. If you'd like to discuss how your ethics and values can be reflected in your investment portfolio and what impact this could have on financial return, please get in touch.

Learn more about Beaufort's ethical portfolios, which combine socially responsible, ethical and environmental considerations with a strategy for capital growth, here.

The cost of university: Parents expecting to pay £17,000

Going to university can be expensive. But not just for the student; parents are expecting to pay out thousands of pounds every year to help their child secure a degree.

Parents anticipate spending £5,721 each year their child is at university, according to research from Lloyds Bank. Over the course of an average three-year degree, it amounts to £17,165. With around half of young people choosing to pursue higher education, it's an expense many households in the UK could be facing.

Just 10 years ago, the figure would have been enough to cover tuition fees and leave some leftover, that's now not the case. Current tuition fees are capped at £9,250. With accessible student loans covering tuition fees, many parents are focussed on the other costs associated with university.

The research found:

- Two-thirds of parents who anticipate sending their child to university expect to support them financially on some level

- Only 14% of parents do not anticipate helping their child financially while they study

- 65% of parents believe they will have to provide support with accommodation costs

- 64% will offer financial help with items essential for study

- 58% expect to pay some or all tuition fees

- 52% will help with travel to and from classes

- 23% are prepared to pay for luxuries

Robin Bullochs of Lloyds Bank said: The costs associated with going to university can mount up quickly, and often it's unexpected costs that rack up the bill making it essential to take some time to consider the many expenses that may arise and budget for how these will be afforded.

The findings suggest parents will face additional outgoings they may not have factored into their budget once teens head to university. Having a fund you've been saving into before they go to university can help spread the cost. For families that have more than one child aspiring to achieve a university education, it could be essential.

With this mind, how can you save for the cost of supporting your child through university?

Junior Individual Savings Account (ISA)

Like their adult counterparts, Junior ISAs offer a tax-efficient way to save.

Each tax year you can add up to £4,260 into a Junior ISA. The interest or return made from a Junior ISA is tax-free. Any money you add to an ISA will be locked away until your child turns 18; at this point, it will be converted into an adult ISA and fully accessible to them.

If you're considering opening a Junior ISA, you have two options: A Cash ISA or Stocks and Shares ISA. Which one is best for you will depend on your attitude to risk and how long you'll invest for.

Junior Cash ISA: If you choose a Cash ISA, the money you put in is safe and you will get a defined amount of interest. That being said, there is a risk that the money won't grow as quickly as inflation, meaning it loses value in real terms.

Junior Stocks and Shares ISA: A Stocks and Shares ISA offers you an opportunity to access potentially higher returns by investing. The return you receive will be dependent on the performance of the underlying investments. It is, of course, possible that the value may temporarily decrease at times.

Children's savings account

There is a range of children's savings accounts to choose from. Often, these types of accounts will offer you more flexibility, such as being able to make withdrawals. However, depending on the terms, this may come with a penalty, for example, losing the specified interest rate.

Children's savings accounts can offer competitive interest rates that will allow the money you deposit to keep pace with inflation in real terms.

Some accounts will specify you put in a certain amount each month or limit contributions. As a result, weighing up the pros and cons of each account is important before you make a decision.

Child Trust Fund

If your child was born between 2002 and 2010, they will have a Child Trust Fund.

The now defunct government scheme aimed to help parents build up a savings account for children. Each account benefited from an initial £250. Some children may have received more as an initial payment and benefited from a further boost when they turned seven.

If you didn't open a Child Trust Fund, the government will have automatically opened one in your child's name. It's estimated that 1.5 million Child Trust Funds are 'lost' or forgotten about. So, it's worth looking into this and you can track down 'lost' accounts here. Once they turn 18, your child will be able to withdraw any money in the account and spend it as they wish.

Even if you haven't added to the account since it was opened, it can provide a starting point to build future savings on. As the Child Trust Funds initiative has since been shelved, you can transfer the money into a Junior ISA account if you choose.

Bare Trust

A Bare Trust is the simplest form of trust. It's where a gift is held for the beneficiary, it can be opened by anyone and then managed directly. The child will be entitled to the money, and able to withdraw it, once they turn 18.

There are several benefits to using a Bare Trust:

- First, the trustee can withdraw money from the Trust before the beneficiary turns 18, so long as it's to benefit the child. It gives you a level of flexibility that some of the other options don't have. For example, you could take out money to pay for college or sixth form fees.

- You can also manage the Trust directly. If you'd like to make specific investments or have a clear risk profile, a Bare Trust might suit your needs.

- Finally, there's no contribution limit; you can add as much as you like to a Bare Trust.

As well as the options above, you may also want to consider saving or investing money in your own name. This is a good option if you don't want your child to have full control and access to the money when they turn 18. It allows you to retain some control over how it's spent and how quickly.

If you want tailored advice on saving for your child or grandchild, we're here to support you. Taking your personal circumstances into consideration, we can help you choose the savings vehicle that's best for you.

Four steps young people should take to improve financial resiliency

Whether you're a young person or you have children and grandchildren, it's important to start building financial resiliency early after research revealed 73% of young adults don't have an emergency fund.

Despite many people in their early thirties planning significant life milestones, such as buying a home or starting a family, research suggests they aren't in a position to do so financially. Across the UK, those aged between 30 and 35 have been identified as one of the least financially resilient groups.

A combination of low savings and a lack of confidence in finance is leading to major life events being put off. With many in this generation focusing on the present, research from LV= suggests that the current generation of 30-year olds aren't preparing for risks they may face in the future.

When looking at the Money Advice Service's (MAS) benchmark for financial resilience, it's a target many in their 30s don't meet. MAS recommends that people should hold an emergency fund of three months' income to weather potential obstacles, such as unexpected bills, illness, or redundancy. However, the LV= report revealed that 73% of those in their early thirties fall short of having 90 days' income saved, this compares to the national average of 56%.

Without financial resiliency, life milestones and security are being harmed for those in their early thirties:

- 24% feel worried about the financial impact on life milestones

- 17% put off major life milestones due to a lack of confidence about their finances

- 43% don't feel confident about handling a personal financial crisis

- 22% don't know how long they would be able to cope financially if they became unemployed

According to Dr David Lewis, an Associate Fellow of the British Psychological Society, seven in 10 under 35s don't properly prepare for future risks because they believe their youthfulness will last forever. It's led to him dubbing the current 4.7 million 30-35-year olds in the UK the 'Peter Pan Generation'.

Dr Lewis commented, There are multiple reasons this age group isn't properly preparing for financial risks. A universal emphasis on the importance of 'staying young' means many people are in a state of denial or avoidance when it comes to facing up to the future. We also tend to talk within - rather than across - generation groups, which encourages us to focus inwardly on the present, not the future.

With people in their thirties likely to be taking significant steps towards milestones where finances are important, bridging the conversation between generation groups could be beneficial. From talking to parents and grandparents to seeking the support of an experienced financial adviser, it could help to identify ways to improve financial resiliency that can be tailored to them.

What steps should you be taking to improve financial resiliency?

If you're searching for ways to improve your financial resiliency now, there are steps that you can start taking. With a plan of action to move forward with, you'll be in a better position to achieve the life goals you want, whether that's to take your first step on the property ladder or become more secure financially as you start a family.

1. Consider the long-term milestones you want to achieve

While there are some common milestones that are on the majority of people's agenda, there's no one size fits all approach. That's why it's important to consider what you want to achieve in the next five or 10 years. Thinking about whether buying a property, getting married, or having children are things you want, means you're able to tailor a financial plan to match these goals.

A simple list with realistic timeframes of when you want to achieve each goal by can help you prioritise where your focus should be and the best option financially.

2. Assess existing income and outgoings

Understanding where you're starting from is crucial for improving financial resiliency. Take the time to assess your current income and outgoings, to work out where you're making mistakes and could be saving more. It's a step that's also important for setting practical dates for when you want to achieve each goal by.

Don't forget to account for any debt you have too, from an existing mortgage to credit cards. Depending on your long-term goals, paying off debt may help you achieve them or access better rates of lending. For example, reducing debt can improve your chances of securing a mortgage offer with a competitive interest rate.

3. Find a savings plan that maximises what you put in

Your savings will grow with you by simply adding to them alone but choosing the right saving plan that benefits from 'free cash' can help speed up your plans. Choosing tax-efficient options, accounts with better interest rates, and government schemes designed to help savers can have a big impact.

The savings plan that is right for you will vary depending on what your long-term goals are. For example, if getting on the property ladder is right at the top of your agenda, a Lifetime ISA (LISA) could be a good option. A LISA is a tax-free wrapper that lets you put in up to £4,000 a year, with a 25% bonus annually to help you build a deposit quicker. While a LISA could work for those working towards securing an early retirement too, a Workplace Pension or an alternative savings account may be a better option and provide more flexibility.

4. Plan for retirement now

With everything else you need to think about, retirement might not even be on your radar yet. However, if you're looking to improve your financial resiliency now, you should take steps to carry that on once you stop working. The earlier you start, the better for retirement planning. If you qualify, staying part of your Workplace Pension is a good place to start. Currently, employees pay 3% of their salary into their pension, with employers contributing a minimum of 2%, these percentages will rise to 5% and 3% respectively in April 2019.

On top of that, you may also want to consider a Private Pension, LISA account, or using a stocks and shares ISA to further build wealth.

To get a better understanding of the steps you could be taking to improve your financial resiliency, contact us.

Could you help your children have a £1 million pension?

Using your gifting allowance effectively could mean you're able to leave your children or grandchildren a significant, tax-free gift behind in the form of a £1 million pension. Discover the steps you can take to reach this goal.

With auto-enrolment now in full force, the topic of saving for retirement has never been more relevant for younger generations. Research has suggested that most people aren't saving enough to achieve the lifestyle they want when they retire, indicating that more than a few future retirees will experience a shortfall, with past research from Hymans indicating a UK-wide shortfall of £5 trillion.

Whether you're a parent or grandparent, using gifting rules and tax efficient saving schemes could help you secure a child's future once they finish work or help get them on to the property ladder.

Previous research from Aegon indicated that 12 million people weren't saving enough to provide the income they require in retirement, with many incorrectly estimating the sums required to generate an income in retirement. The firm's analysis found that people on average earnings required a pension of £301,500 to maintain their lifestyle in retirement. Future retirees that are planning to use their years after work to travel and explore new hobbies without the restrictions of work will need significantly more.

With the rising cost of living, the challenges of getting on the property ladder and student debt increasing, helping children and grandchildren experience long-term financial security is becoming a common goal. The good news is that with a bit of forward planning it is possible to help your child or grandchild have the means to purchase a property in adulthood or even secure them a £1 million pension.

Rather than leaving your loved ones an inheritance, which may be subject to Inheritance Tax (IHT), you can use your money to help children build wealth while you're alive. It gives you an opportunity to firstly leave a larger legacy and to see your loved ones enjoy your generosity while you're still with them. With IHT reaching record levels last year, it's an option that's worth exploring.

Laura Suter, Personal Finance Analyst at investment platform AJ Bell, said: Parents or, potentially more realistically, grandparents can save on their inheritance tax bill and pass substantial sums to their children or grandchildren by making use of lucrative annual gifting allowances.

Figures released recently showed record levels of inheritance tax were paid last year, topping £5.2 billion. As more and more people are caught in the net of inheritance tax, it's more important than ever to make use of the allowances the Government hands you.

Using your gifting allowance

If you're worried about your children and grandchildren facing a significant IHT bill when you pass away, using your gifting allowance wisely can help to put your mind at ease. It's a way for you to pass on substantial sums over time without being subject to IHT.

To begin with, your annual gifting allowance is £3,000, this is money that will always be free from IHT. Should you decide to gift over £3,000 annually, there's the seven-year rule to think about. Should you die within seven years of a monetary gift being received that went beyond the gifting allowance, IHT may need to be paid.

By making full use of the annual £3,000 gifting allowance to help children, AJ Bell has calculated that families could save £43,000 in IHT if both parents and grandparents use it to build wealth over an 18-year period.

What to do with the gifted money

According to the research from AJ Bell, if both parents and grandparents maximise their gifting allowance from the first year of a child's life right through to reaching 18, the child will have accumulated £108,000 before they even leave compulsory education. With this in mind, how should you hold this money to ensure it benefits them in the long-term?

There are two potential options to consider, a pension and a Junior ISA, depending on how you want the money to be used and accessed.

Junior pension

You can start saving for your child's future right away with a pension.

For children, contributions to a pension benefit from 20% tax relief up to a maximum annual contribution of £3,600. That means if you contribute £2,880 on behalf of your child or grandchild, they will receive a tax relief of £720 (which is effectively 'free money'). AJ Bell's figures show you end up with a sum of £64,800 over an 18-year span. Assuming returns of 5% after charges, your child's pension will have reached £105,197 before they start their working life.

Without any further contributions, AJ Bell's figures indicate it will take 46 years for the pension to reach the £1 million milestone, allowing your child to comfortably retire and enjoy their later years by the age of 64.

Of course, there is no guarantee that this will be the actual amount that will be in your child's pension. A range of different factors, including rate of return and charges levied, have an impact and need to be considered.

Laura Suter comments: Given the growing savings gap in the UK, a £1 million pension pot is an amazing thing to create for a child and gives them one less thing to worry about as they struggle with student debt.

Of course, with the right financial knowledge instilled, the child's pension should continue to grow, for example, through workplace contributions. However, one area to be mindful of is ensuring that they don't end up breaching their Lifetime Allowance on their pension. This is currently set at £1.03 million but it is a figure that will rise alongside the cost of living as it is index linked.

Junior ISA

If you want to ensure your child or grandchild has a significant financial buffer before they reach the age of 18 but don't want the restrictions of a pension, a Junior ISA could prove to be the better option for you. Rather than having to wait until retirement age, the child would be able to access the money once they reach adulthood, making it an excellent option for providing support to get on the housing ladder.

Junior ISAs can be used from birth up to the age of 18, with an annual contribution limit of £4,260. If you only used your £3,000 gifting allowance to make yearly deposits in an account that benefitted from 5% interest rates, the sum would total £87,664, which would be tax free to withdraw. Taken out at 18, the Junior ISA would provide a sizeable deposit for a home. Alternatively, if the account was left accumulating interest with no further deposits for a further decade, it would reach £144,383, AJ Bell's calculations show.

Get in touch with us to discuss the most tax efficient way to gift and maximise your legacy with securing your children or grandchildren's future in mind.